New IR35 Rules Explained: How the Government Is Tackling “Disguised Employment” in the Security Industry

IR35 legislation continues to reshape the UK contracting market in 2026, with businesses across the private security industry, cyber security sector, and wider security services industry facing growing pressure to ensure contractors are genuinely self-employed rather than operating in what HMRC describes as “disguised employment.”

The off-payroll working rules were introduced by the government to prevent individuals from working like permanent employees while benefiting from the tax advantages of self-employment through limited companies. As a result, many UK security companies, security recruitment agencies, and contractor-led businesses are reviewing their IR35 compliance procedures and employment status assessments.

From cyber security consultants and surveillance specialists to close protection operatives, CCTV professionals, event security staff, and security project managers, IR35 remains one of the most important compliance issues affecting the modern security workforce. Industry experts believe that security contractor compliance and HMRC employment status checks will continue to be a major focus throughout 2026 as demand for specialist security professionals continues to grow across the UK.

What Is “Disguised Employment”?

According to HMRC, disguised employment occurs when a worker operates through a limited company or intermediary — often referred to as a personal service company (PSC) — while, in reality, working in much the same way as a permanent employee within an organisation. Within the UK security industry, this can affect contractors working across physical security services, cyber security, CCTV monitoring, close protection, mobile patrols, and corporate security operations.

While the individual may technically be classed as self-employed, HMRC assesses whether the day-to-day working relationship more closely resembles standard employment. This has become a growing issue for security contractor compliance, particularly for businesses relying heavily on subcontracted or freelance security professionals.

The government argues that, prior to the introduction of the off-payroll working rules, some contractors were able to reduce their Income Tax and National Insurance contributions despite effectively carrying out employee-style roles for long periods of time. In some cases, contractors worked exclusively for a single organisation, followed company policies and working hours, and operated under direct supervision while still benefiting from the tax advantages associated with limited company contracting.

For many UK security companies and security recruitment agencies, this has increased the importance of proper IR35 compliance and employment status assessments. Businesses operating within the private security sector are now being encouraged to regularly review contractor arrangements, working practices, and contractual terms to reduce the risk of HMRC investigations.

IR35 was introduced to close what HMRC viewed as a loophole within the tax system and to ensure workers performing similar roles pay broadly similar levels of tax, regardless of whether they are engaged as employees or through intermediary companies. The legislation continues to impact a wide range of security roles, including cyber security consultants, surveillance specialists, event security staff, security project managers, and close protection operatives.

Under the legislation, contracts and working arrangements are assessed to determine whether a worker is genuinely self-employed or should instead be treated as employed for tax purposes. HMRC may examine several factors during an assessment, including the level of control exercised by the client, whether the contractor can provide a substitute, the degree of financial risk involved, and how integrated the individual is within the organisation.

Supporters of the legislation argue that the rules help create fairness across the workforce and prevent tax avoidance, while critics claim the reforms have increased uncertainty within the contractor market and reduced flexibility for both businesses and highly skilled freelance professionals working throughout the security services industry.

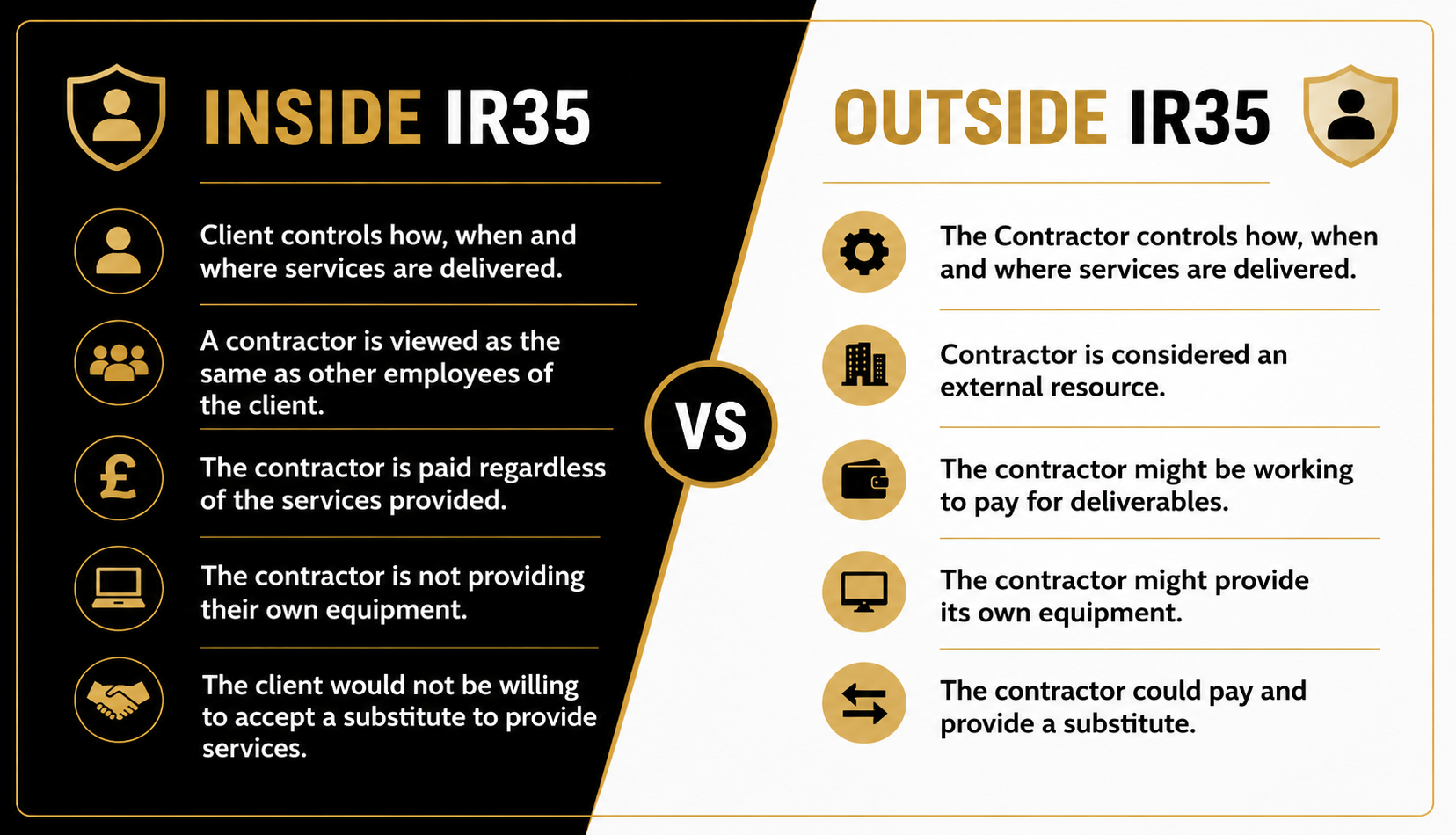

Inside vs Outside IR35

Contracts considered “inside IR35” are taxed in a similar way to permanent employment, meaning contractors are typically paid through PAYE with Income Tax and National Insurance contributions deducted at source. Within the UK security industry, this can affect a wide range of professionals including security guards, cyber security contractors, CCTV specialists, close protection operatives, and security consultants. In many cases, contractors working inside IR35 may also see reduced take-home pay compared to traditional limited company contracting arrangements.

By contrast, contracts deemed “outside IR35” allow contractors to continue operating as genuinely self-employed businesses through their limited companies. These arrangements often provide greater flexibility, control over working practices, and the ability to manage income through standard company structures. Many professionals working within the private security sector and wider security services industry aim to secure outside IR35 contracts where possible.

Under the off-payroll working rules, medium and large private-sector organisations are generally responsible for determining a contractor’s IR35 status rather than the contractor themselves. Businesses must assess whether the working relationship reflects genuine self-employment or resembles standard employment and then provide a Status Determination Statement (SDS) outlining their decision.

For many UK security companies, security recruitment agencies, and businesses using subcontracted security professionals, these compliance requirements have become increasingly important. Firms operatingwithin physical security services, cyber security, surveillance, event security, and risk management are being encouraged to regularly review contractor arrangements and ensure proper IR35 compliance procedures are in place.

Industry experts say the shift in responsibility has led many organisations to adopt increasingly cautious approaches to compliance, particularly within specialist sectors such as security, cyber security, and technical consultancy, where contract-based work remains common. As HMRC continues to increase scrutiny around employment status checks, security contractor compliance is expected to remain a major issue throughout 2026.

Security Industry Feeling the Impact

Many organisations have adopted increasingly cautious approaches to IR35 compliance in an effort to avoid potential HMRC investigations, financial penalties, and unexpected tax liabilities. Since responsibility for determining IR35 status shifted to medium and large private-sector businesses, some companies — including firms within the UK security industry — have responded by placing contractors inside IR35 by default rather than carrying out individual assessments on a case-by-case basis.

Industry recruiters say this approach has created growing challenges when attempting to attract and retain experienced freelance professionals, particularly within highly specialised areas of the private security sector where contract-based work has traditionally been common. Some security contractors are reportedly declining inside IR35 roles altogether, choosing instead to seek outside IR35 opportunities, overseas contracts, or permanent positions offering greater financial stability.

Recruitment specialists say the impact has been particularly noticeable across areas including:

Cyber security

Infrastructure protection

Security consultancy

Surveillance operations

Risk management

Technical security projects

Businesses operating across the wider security services industry often rely on highly skilled contractors for short-term projects, incident response work, compliance programmes, cyber security support, and specialist technical services. However, some organisations have reported increased competition for experienced professionals as the pool of contractors willing to work inside IR35 continues to shrink.

Experts believe this ongoing shift could continue to affect recruitment across both physical security services and the cyber security sector throughout 2026, particularly as demand for qualified security professionals remains high across the UK.

HMRC Looking Beyond the Contract

In the UK security industry, IR35 compliance is becoming an increasingly

important issue for contractors, subcontractors, and security firms alike.

While many businesses focus heavily on the wording of contracts, tax

specialists and legal experts continue to warn that HMRC will often look

far beyond the written agreement when assessing employment status.

HMRC investigations frequently examine the actual working relationship

between the contractor and the client to determine whether an individual

is genuinely operating as an independent contractor or functioning more like

an employee. This means that even a ell-written contract may not be enough if day-to-day practices suggest otherwise.

Key areas HMRC may review include:

Control over the work – who decides how, when, and where duties are carried out

Substitution rights – whether contractors can genuinely provide a substitute worker

Supervision and management – the level of oversight applied during assignments

Financial risk – whether the contractor bears business-related costs or liabilities

Integration into the organisation – whether the individual appears embedded within the client’s internal structure

For security companies operating within regulated sectors, critical infrastructure, construction sites, corporate environments, or high-security operations, these factors can become particularly significant. Contractors working fixed patterns, wearing company uniforms, using client-issued equipment, or being managed in the same way as permanent staff may face greater scrutiny during an HMRC review.

Industry advisors are therefore encouraging security firms to ensure that operational practices accurately reflect the terms outlined in contracts. This includes maintaining clear contractor independence, documenting working arrangements properly, and regularly reviewing compliance procedures to reduce potential IR35 risks.

Failure to align operational reality with contractual wording can expose businesses to substantial tax liabilities, penalties, and reputational damage. As HMRC continues to increase enforcement activity across labour-heavy sectors, security firms are being urged to take a proactive approach to employment status compliance.

Why IR35 Compliance Matters in the Security Industry?

The private security sector often relies on flexible staffing models, subcontractors, and short-term deployments to meet operational demands. However, this flexibility can create uncertainty around employment status if contracts and working practices are not carefully managed.

Security businesses should regularly assess:

Contractor onboarding procedures

Shift allocation and rota management

Equipment and uniform policies

Reporting structures and supervision levels

Substitution and assignment flexibility

Record keeping and compliance documentation

By reviewing these areas, firms can better demonstrate genuine contractor relationships while reducing exposure to HMRC investigations.

Experts warn that IR35 decisions are not based solely on written agreements.

HMRC may also examine the day-to-day working relationship between the contractor and client, including:

Who controls the work

Whether substitutes can be provided

Level of supervision

Financial risk

Integration into the organisation

Security firms operating in regulated or high-security environments are being advised to ensure operational practices align with contractual terms.

Check Whether IR35 Applies to You

Contractors, recruitment agencies, and businesses operating within the UK security industry should regularly assess whether the IR35 off-payroll working rules apply to their working arrangements. Understanding your employment status is an important part of maintaining proper IR35 compliance and reducing the risk of future HMRC investigations.

Businesses using subcontractors or self-employed operatives within the private security sector, including physical security, cyber security, CCTV monitoring, mobile patrols, and event security services, are being encouraged to review current contractor agreements and operational practices carefully.

The official government guidance explains how HMRC assesses employment status, who is responsible for making IR35 determinations, and the potential financial risks associated with non-compliance, including tax liabilities and penalties.

Contractors and employers can review the official guidance here:

HMRC IR35 Guidance and Off-Payroll Working Rules

The guidance covers:

Employment status assessments

Off-payroll working legislation

Contractor and employer responsibilities

IR35 tax compliance requirements

HMRC investigation processes

Risks linked to incorrect IR35 determinations

As HMRC contractor compliance checks continue across multiple sectors, security companies and contractors are being advised to regularly review their working practices to ensure they align with current UK contractor regulations and IR35 requirements.

Ongoing Debate Across the Industry

IR35 continues to be a major talking point across the UK contractor market, particularly within the security industry where flexible staffing models are widely used. From physical security services to cyber security contractors, businesses across the sector are continuing to assess how the latest IR35 regulations affect recruitment, compliance, and day-to-day operations.

Supporters of the legislation argue that the rules help create greater fairness within the UK tax system by preventing individuals from benefiting from the financial advantages of self-employment while effectively working as employees. HMRC maintains that the off-payroll working rules are designed to ensure contractors and employees pay similar levels of tax where working arrangements are comparable.

Critics, however, believe the legislation has created uncertainty across the wider UK contractor market. Many security firms and recruitment agencies argue that the reforms have reduced flexibility when sourcing specialist expertise at short notice, particularly within the growing cyber security sector, mobile patrol services, event security, CCTV monitoring, and risk management roles.

Industry experts have also warned that cautious IR35 assessments could discourage experienced contractors from accepting assignments, potentially increasing recruitment pressures across the private security industry and wider security staffing sector.

As demand for qualified professionals continues to rise across both physical and cyber environments, IR35 compliance in the security industry is expected to remain a major issue for contractors, agencies, and employers throughout 2026 and beyond. Businesses are being encouraged to regularly review contractor arrangements and maintain strong security company compliance procedures to reduce potential HMRC risks.